It's no secret that there are benefits to the S corp tax structure for therapy practices.

One of the biggest? The chance to reduce your tax burden and save more money each year.

Switching your practice to an S corporation also costs money. So how do you know if it’s worth your while?

Below you’ll find three examples demonstrating the way an S corp structure saves you money, and how much you can expect to save in different situations.

But first, a quick review of the basics.

How does switching to an S corp save your therapy practice money?

When you’re a sole proprietor, 100% of your income is subject to federal self-employment tax. It’s a flat tax rate of 15.3%, which accounts for 12.4% for social security and 2.9% for Medicare.

When your practice is an S corporation, you only pay the equivalent of self-employment tax (FICA, the Federal Insurance and Withholdings Act payments, encompassing Social Security and Medicare) on money you earn as an employee.

To cover FICA, 7.65% of your income is withheld by your employer, while your employer matches the amount with their own 7.65% contribution.

In that case, since you’re your own employer, you end up paying 15.3%—equivalent to self-employment tax—on the salary you pay yourself as an employee.

If these numbers and taxes have your head spinning, check out our article on how to pay yourself as a therapist to get a grounding in the basics.

So where do the tax savings come from? From the fact that you only pay yourself a portion of your total income as salary. For instance, your practice might earn $100,000 per year, but you only pay yourself $80,000 in salary. That leaves $20,000 that isn’t subject to self-employment tax at a rate of 15.3%.

A quick back-of-the-envelope calculation shows you save $3,060 in taxes you’d otherwise pay on that $20,000.

There may be other ways to save money by electing S corp status for your practice, but reducing your self-employment tax burden is the biggest one—and it’s the one covered by the examples below.

A word about reasonable salary: If you plan to hire yourself as an employee and enjoy tax savings as a result, you’re legally required to pay yourself a reasonable salary. Check out our article How to Calculate a Reasonable Salary as a Therapist for more info.

{{resource}}

When should you consider switching your therapy practice to an S corp?

Not all practices benefit from switching to S corp status. Because of the cost of becoming an S corp, and the fact that you can only begin to realize tax savings when your salary is significantly less than your total income, it doesn’t make sense to switch business structures until you reach a certain income threshold.

Different accountants have different ideas when it comes to what that threshold should be. At Heard, based on our experience handling bookkeeping, accounting, and taxes for thousands of therapists, we recommend a threshold of $100,000 annual net income.

If your practice’s annual net income is less than $100,000, switching to an S corp is unlikely to significantly benefit you, and may cost you more money in the long run.

To run the numbers yourself, check out our S Corp Tax Savings Calculator for Therapists.

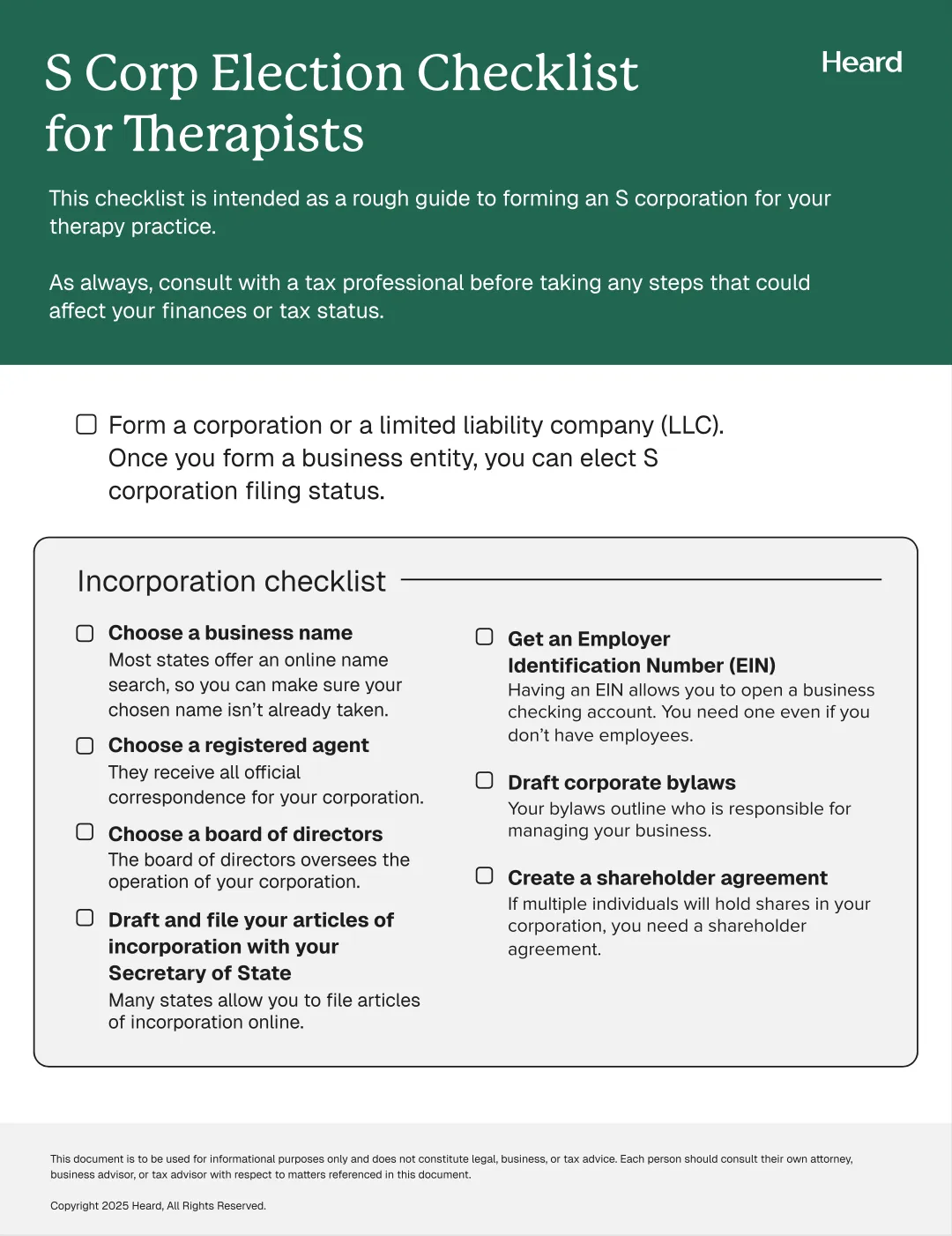

How do you switch your therapy practice from a sole prop to an S corp?

Roughly, the steps to converting your sole prop to an S corp look like this:

- Incorporate your business at the state level by registering it with your Secretary of State (or equivalent).

- You file a federal S corporation election with IRS Form 2553. The deadline is the 15th day of the third month of the first tax year you incorporate. In most cases, this is March 15, unless you incorporate mid-year.

- You maintain LLC and S corp status by meeting state and federal filing and fee requirements each year.

At the level of state taxes and state business registration, your practice becomes an LLC. At the level of federal tax filing, it’s an S corporation.

For a deeper dive, check out our Complete Guide to LLCs and PLLCs for Therapists and our Complete Guide to S Corporations for Therapists.

How much does it cost to switch your therapy practice from a sole prop to an S corp?

It costs money—anywhere from $50 to $800, depending on your state—to register an LLC. Electing S corp status with the IRS costs money, too, if you pay an accountant to do it for you. S corp set up fees can range to $1,000 or more.

On top of that, you should expect to pay higher accounting and bookkeeping fees for your practice once it goes from being a sole prop to being an S corp. S corp bookkeeping and tax filing is more complex, and takes more time (and expertise) to tackle.

Finally, once you hire yourself on as an employee, there are additional outlays: the cost of a payroll platform for your therapy practice, plus state-level fees like unemployment insurance and workers’ compensation contributions.

For a complete rundown—and some hard numbers—check out How Much Does it Cost Therapists to Switch to an S Corp?

The good news is that, despite these additional costs, provided you meet the income threshold recommended above, S corp status can still save you a substantial amount of money each year.

{{resource}}

How much you save by switching to an S corp: 3 examples

These three, simplified examples of hypothetical therapy practices illustrate how practices can save money on taxes by electing S corp status.

The three examples:

- A practice based in California with a net income (before accounting for employee wages) of $150,000

- A practice based in New York State with a net income (before accounting for employee wages) of $120,000

- A practice based in Georgia with a net income (before accounting for employee wages) of $100,000

The different locations of these practices account for the difference in wages paid to their owners. As an S corp owner, you’re required to pay yourself a reasonable salary, on par with the average earnings of other therapists in your area. Average earnings of therapists vary from one region to the next, and so will the amounts you can set for reasonable wages.

Example #1: California

* After S corp annual operating costs ($4,400): $6,310

Example #2: New York State

* After S corp annual operating costs ($4,400): $4,015

Example #3: Georgia

* After S corp annual operating costs ($4,400): $1,720

{{resource}}

The three examples explained

Each table shows how much a hypothetical practice could save on federal self-employment tax if it elected S corp status and paid the owner as an employee.

Federal self-employment tax is charged at 15.3% of taxable income. For employees, the equivalent is 7.65% (employee contribution) and 7.65% (employer contribution).

Net Income is the total taxable income (before employee wages) earned by the practice, after business expenses have been deducted.

Owner Wages are, in the event the practice elects S corp status, the annual amount paid to the wonder of the practice as an employee. Only these wages are subject to self-employment tax (technically a total of the employee and employer’s FICA contributions, but equal to the 15.3% otherwise charged on self-employment income).

Pass-through Profit is the amount of profit earned by the practice either as a sole prop or an S corp. For a sole prop, this is equivalent to the net income. For an S corp, it’s equivalent to net income minus employee wages.

Amount Subject to Income Tax is the portion of net income taxed at the sole prop or S corp’s income tax rate. Whether your practice is a sole prop or an S corp, 100% of its net profits are taxable. In the case of a sole prop, you pay income tax on your total self-employment earnings. In the case of an S corp, you pay income tax on both your self-employment earnings (the S corp’s total earnings after deducting employee wages) and the wages you earn as an employee. In either case, the total taxable amount is the same.

The note below each table is a calculation of total tax savings after taking into account an average S corp operating cost of $4,400.

This $4,400 covers costs that would not normally be paid by a sole prop, such as increased accounting, bookkeeping, and tax filing fees. For a full breakdown of the cost of forming and maintaining an S corp, see How Much Does it Cost Therapists to Switch to an S Corp?

The takeaway

In every instance where a hypothetical therapy practice is above the $100,000 net income threshold, the practice saves money by being taxed as an S corp, even after taking into account the added cost of maintaining S corp status.

To get a better sense of why the $100,000 threshold is important, here’s the Georgia therapy practice example, but with an income of $80,000 instead of $100,000:

* After S corp annual operating costs ($4,400): $ -1,340

In this case, the practice actually loses money by electing S corp status. After taking into account the extra cost of running an S corp, the practice is at a $1,340 deficit compared to where it would be if it operated as a sole proprietorship.

These are simplified examples. State and municipal taxes—including annual franchise tax and/or filing fees for an LLC, PLLC, or equivalent business structure—all affect the bottom line. Before deciding to elect S corp status, consult with a CPA.

—

How much could your practice save by electing S corp status? Find out with our S corp tax savings calculator for therapists.

This post is to be used for informational purposes only and does not constitute legal, business, or tax advice. Each person should consult their own attorney, business advisor, or tax advisor with respect to matters referenced in this post.

Bryce Warnes is a West Coast writer specializing in small business finances.

{{cta}}

Manage your bookkeeping, taxes, and payroll—all in one place.

Discover more. Get our newsletter.

Get free articles, guides, and tools developed by our experts to help you understand and manage your private practice finances.