Most therapists in private practice are in debt.

According to our 2024 Financial State of Private Practice Report, the majority of therapists surveyed—60 percent—were still paying off their student loans.

But that’s just one type of debt. Besides the cost of their education (plus interest), many therapists have mortgage payments, car payments, credit card debt, and business loans to deal with.

So what do you do when you’re overwhelmed by the cost of payments, when it feels like you’ll never pay off your debt—and, in the meantime, you have to run your own practice?

Here are some tried and true strategies for paying off debt as a therapist, and steps you can take if your debt becomes unmanageable.

{{resource}}

Assess your debt

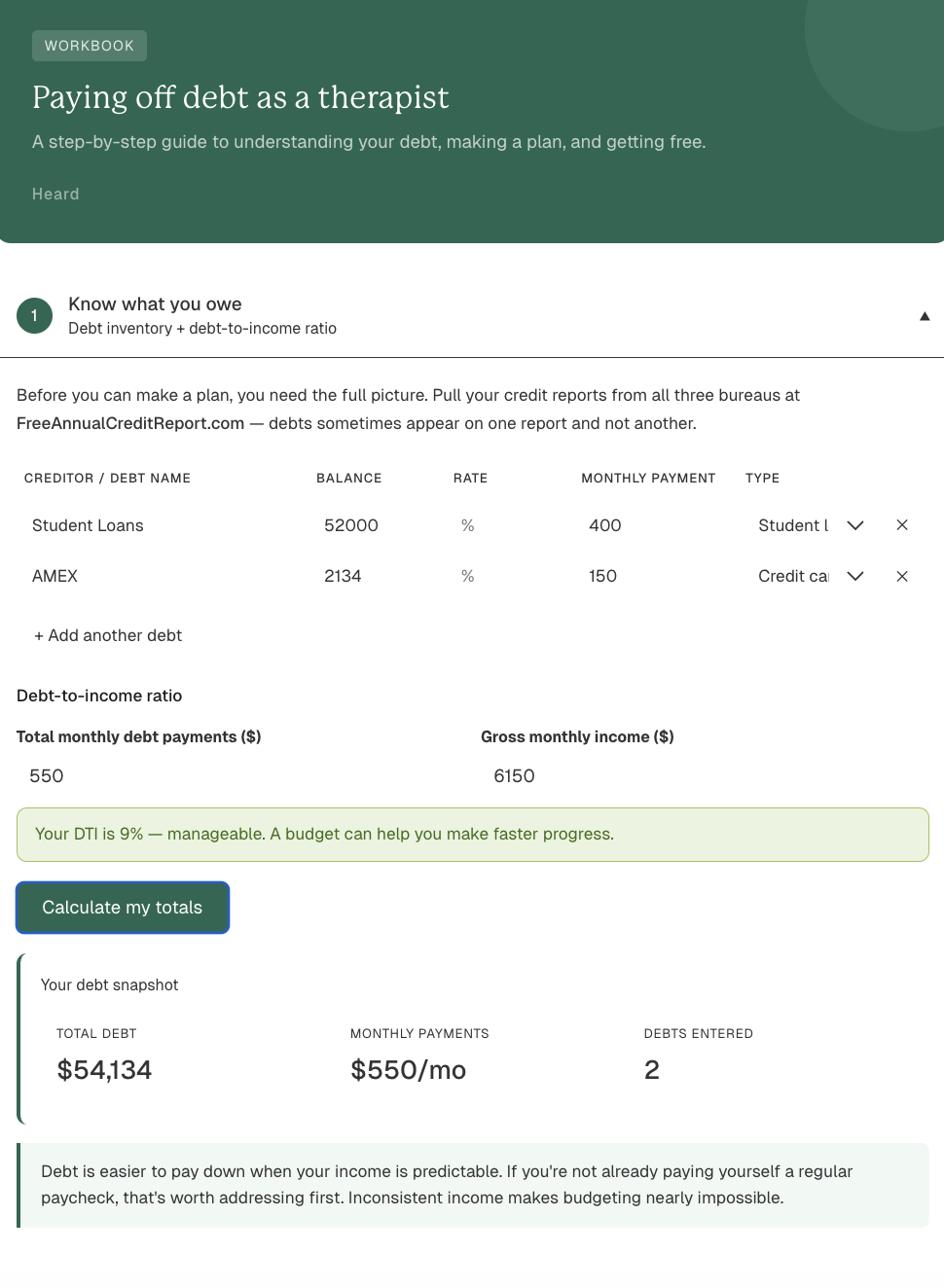

Before you can create a plan for paying off your debt, you need to figure out how much you owe in total and the creditors to whom you owe it. That gives you a big-picture view of all the debt you need, eventually, to pay off.

The next step is to calculate the impact debt payments have on your cash flow so you can put together a sustainable monthly budget.

Calculate your total debt

To start calculating your total debt, request credit reports from the three major credit reporting bureaus: TransUnion, Equifax, and Experian.

Some debts you owe will appear on one credit report, but not on another. That’s why it’s important to request reports from all three bureaus, since no single bureau is guaranteed to have the whole picture. You can request reports using FreeAnnualCreditReport.com.

Review these reports to make sure they include all of your debts to all of your creditors. If anything is missing, go through your personal files to find the information you need, or contact a creditor directly.

Once you have the total amount you owe for each of your debts, write each one down on a sheet of paper (or in a spreadsheet) and add it up. This is the total amount you owe.

Calculate your debt-to-income ratio

Your debt-to-income ratio represents the percentage of your monthly income you currently spend on debt payments.

To calculate this ratio, go through your bank statements for the past several months. Create a list of debt payments made each month and add up the total amount.

Then calculate your monthly income. This may be tricky, depending on how you pay yourself with your therapy practice.

For example, if you’re not in the habit of paying yourself regular weekly or biweekly owner’s draws, but rather take cash out of your business banking account as it’s earned—or whenever you need it—your income may vary from one month to the next.

If necessary, add up your total monthly income for multiple months, then divide the amount by the number of months to find a monthly average.

Once you have your total monthly payments and your total monthly average, you can calculate your debt-to-income ratio by dividing your monthly debt payments by your gross monthly income.

Example: Your total monthly debt payments come to $1,400. Your monthly gross income is $4,000. If you divide 1,400 by 4,000, the result is 0.35. Your debt-to-income ratio is 35%.

Assessing your debt-to-income ratio

According to the Consumer Financial Protection Bureau, debts are likely to become unmanageable at ratios of 43% or higher. Meaning, once you hit 43%, you’re likely to struggle making your monthly payments while covering other personal expenses.

This is not a one-size-fits all number, however. You may already be struggling to make your monthly payments, but after crunching the numbers, find your debt-to-income ratio is only 35%. That could be a result of having a lot of monthly expenses to cover—for instance, if the cost of living in your area is high, or if you have dependents.

It could also be the result of faulty budgeting. If income from your therapy practice is variable, and you don’t stick to a well-planned monthly budget, you may find yourself overspending on personal expenses when your income is high and struggling to make ends meet when it’s low.

In that case, planning a sustainable monthly budget could be the answer to your problem.

Make a personal budget

Sitting down to create a personal monthly budget, or to adjust your current monthly budget so you’re better able to cover debt payments, serves two functions:

- It helps you create a plan for meeting your debt obligations and eventually paying off your debt.

- It can serve as the proverbial canary in the coal mine if your debt has reached unmanageable levels.

The first function is pretty self explanatory. The second may not be so obvious.

The canary in the coal mine

If you start building a monthly budget, but the numbers just don’t add up—you can’t find any way to cover your monthly personal expenses while also making monthly debt payments—it’s a sign your debt has become unmanageable.

It’s possible to carry an unmanageable amount of debt but still cover your monthly payments. You may find yourself using a credit card to cover monthly expenses, dipping into long-term savings to cover debt payments, or holding off on debt payments (paying them late) until you have cash in hand to cover them.

In a word, you’re always shuffling money around, but the end result is that your debt grows (or your savings diminish) and your credit score deteriorates as you struggle to keep up.

That’s where making a budget can serve as a wake-up call. Once you have the hard numbers in front of you, and you realize there’s no way you can service your debt while covering monthly expenses, you know your debt is unmanageable. It’s time to look at alternative strategies for paying it off or reducing the load.

But it’s not all doom and gloom. You may discover your debt is totally manageable if you reduce unnecessary monthly expenses. A solid monthly budget can point you down the road to a debt-free future.

How to build a monthly personal budget

Even if it seems intimidating at first, making a budget is fairly straightforward.

In fact, if you’ve already gathered the information you need to assess your debt—your monthly expenses, your monthly debt payments, and your monthly income—you already have everything you need to build your budget.

Here’s how to do it.

1. List your monthly income.

If you have multiple income streams, break it up according to income stream.

2. List your monthly expenses.

These include expenditures like utilities, groceries, gas, insurance, and contributions to retirement funds. But be sure to include items for entertainment (dining out, digital subscriptions, vacation savings), and for irregular expenses (clothes purchases, home repairs, doctor bills). Even if (for instance) you don’t buy yourself new clothes each month, determine an amount to contribute to a clothing fund so you have cash on hand when the time comes.

3. List your monthly debt payments.

This includes everything from your mortgage, car, and student loan payments to your credit card payments and personal IOUs.

4. Subtract your total monthly expenses and debt payments from your income.

This section of your budget should ideally come to zero. If you have extra funds left over, assign them to expenses (e.g. monthly contributions to a savings fund) or debt payments (e.g. paying down a credit card). The goal is to account for every penny, so you know where all of your income is going each month.

If you find it a struggle to create a monthly budget on paper, consider using an app like You Need a Budget (YNAB). A budgeting app may add to your monthly expenses—since most charge subscription fees—but it’s a worthwhile investment if it allows you to build a budget that meets your needs.

Report on your budget

It’s all well and good to have a monthly budget, but it won’t work for you long term if you don’t report on it.

A budget doesn’t just tell you how to spend your money, it tracks how you spend it. Update your budget each month, marking off expense and debt payments as you make them and recording your income.

Not only will you be able to confirm that you’re meeting your budgeting goals, you’ll be able to spot any line items in your budget that need adjusting.

Review and adjust your budget

Set a goal to periodically review your budget and make adjustments as needed.

Monthly expenses change, and so do debt payments. Your income may increase or decrease. All of these have an impact on your budget. Keeping your budget up to date guarantees that you’re always tuned in to your monthly spending and that you can account for every dollar.

Cut yourself a paycheck

If you want to make budgeting for personal expenses much easier, and significantly increase your chances of paying off your debt, you need to cut yourself a regular paycheck.

That is, if you’re in the habit of taking earnings from your therapy practice’s business account irregularly, you’ll have a hard time setting a monthly income for your budget. One month, you may find yourself short on cash to cover expenses; the next, you may have more than you know what to do with.

Taking regular, fixed owner’s draws—or paying yourself as an employee—on a weekly or biweekly basis is the fastest route to maintaining a monthly budget that works.

To get started, check out our guide to paying yourself as a therapist.

Trim back expenses

When you first make your budget, and when you periodically review it, keep on the lookout for ways you can reduce your expenses.

For instance, if you’re serious about paying off your debt, you may decide to forego a vacation this year and use the money instead to pay off a credit card.

Or by taking advantage of coupons and sales, or buying certain items in bulk, you could lower your grocery bill.

Every dollar you save on monthly expenses is a dollar you could be spending to pay down your debt. And depending on the debt repayment strategy you follow (covered below), you could see your debt burden shrink faster than you expected.

{{resource}}

Set a goal for paying off debt

Setting a goal for becoming debt-free can help motivate you to make changes to your spending now that will pay off in the future. And once you have a goal—or goals—to work towards, making debt payments feels less like treading water and more like swimming for the shore.

Depending on the types of debt you have, it may make sense to break down your one, major goal—becoming debt-free for good—into multiple goals in two categories: short-term and long-term goals.

Setting short-term goals

While paying off some debts, like your mortgage or even your student loan, may take decades, others may be eliminated much sooner.

Take an inventory of debts you can reasonably hope to pay off in five years or less. Examples include credit cards, lines of credit, and financing for household items like appliances, electronics, and furniture.

Then calculate the total amount of time it will take to pay off each debt based on your current debt payments.

If you have room in your budget, you may increase your payments on particular debt in order to wipe it out sooner. Different strategies for prioritizing which debts you pay off first are covered in the next section.

Whatever approach you use, the important thing is to set an “expiry date” for each debt. Not only does that give you something to look forward to, it’s an important reminder that debt is not forever. There is an end in sight.

Setting long-term goals

Long-term goals, such as paying off your mortgage or your student loan, are by their nature less immediately rewarding than short-term goals.

Still, tracking certain milestones—and celebrating them—can help break the job down into digestible pieces.

For instance, you might make a note of when your mortgage will be one-quarter paid off, then two-quarters, and so on. Or you could set a date for paying down half the principal on your student loans.

By opting for accelerated mortgage payments, or increasing the amount you pay on your student loan each month, you can speed up the process. But keep in mind that putting an extra $100 towards your $50,000 student loan each month will have less of an impact, proportionately, than paying an extra $100 on your $2,500 credit card debt.

How you prioritize different debts depends on your personal preferences and money mentality, and the debt strategy you choose to follow.

Consider different debt repayment strategies

A debt repayment strategy serves as your guide for allocating funds to your various debts.

Naturally, if your budget leaves you with no wiggle room—if the best you can do each month is to make the minimum necessary payments on your debts—you may not have the luxury of choosing a debt repayment strategy.

But once you have more money to spend on debt repayment—either because of increasing income as your therapy practice grows, or because you’ve reduced your monthly expenses—it’s time to put that money to work.

Credit counsellors commonly recommend choosing one of three strategies for paying off debt: the debt snowball, the debt avalanche, and lower credit utilization.

The debt snowball

With the debt snowball strategy, you focus on paying off your smallest debt first.

The main benefit of this method is psychological. Choosing the smallest debt to pay off first—and then the next smallest, and so on—means you’re quickly rewarded with the satisfaction of meeting short-term goals.

For instance, you may already know that it will take years of work before you pay down your $50,000 student loan debt. But if you use the debt snowball strategy, you may be able to pay off your $2,500 credit card in a matter of months.

To hit this goal, you keep all other debt payments at their bare minimum, while spending as much as you can afford paying down your smallest debt.

With one less outstanding debt to worry about, and with extra funds in your monthly budget freed up once that debt is gone, the $50,000 burden doesn’t feel quite so heavy any more. You may feel more motivated to continue paying off your other smaller debts, building up momentum—like a rolling snowball—as you go.

The main drawback to this approach is that the debt you pay down first isn’t necessarily the one that’s costing you the most money in interest payments. If your $2,500 credit card debt has an APR of 24.99%, but your $10,000 credit card debt has an APR of 28.99%, then in the long run you’ll end up paying more in interest.

The debt avalanche

Whereas the debt snowball focuses on emotional rewards for eliminating debt, the debt avalanche method focuses on the slightly more cerebral pleasure of reducing how much you pay in interest payments.

With this method, you focus on paying off the debt with the highest interest rate—that is, the one that ends up costing you the most money in the long run. Following this approach, you would prioritize your $10,000 credit card debt with an APR of 28.99% over your smaller, $2,500 credit card debt of 24.99%.

The result is that you may spend longer completely paying off a particular debt, but you’ve ended up saving more money.

Lower credit utilization

The lower credit utilization strategy doesn’t have a fun name like the debt snowball or the debt avalanche, but it could be the right choice if you want to improve your credit rating ASAP.

Your credit utilization is the amount of your available credit you make use of. For instance, if you have a $7,000 limit on your credit card, and your debt is $2,500, your credit utilization is lower than it would be if you owed $5,000 on the same card.

Lower credit utilization typically contributes to a better credit score. If you decide that you’re less interested in paying off all your debt so much as improving your credit score in order to access more credit on more favorable terms—for instance, if you’d like to qualify for a mortgage—then the lower credit utilization may be the best approach.

Improving your credit score may also allow you to qualify for a debt consolidation loan, covered below.

With this strategy, you focus on paying down the debt that has the largest credit utilization. For instance, suppose you owed $5,000 on a credit card with a limit of $7,000, and $12,000 on a line of credit with a limit of $20,000.

Since $5,000 is about 70% of $7,000, and $12,000 is 60% of $20,000, you’d prioritize paying down your credit card first. In a relatively short amount of time, you may be able to significantly reduce your credit utilization on your credit card, which in turn impacts your credit score.

If your aim is to improve your credit rating as part of a long-term goal, like buying a house, consult with a financial advisor, credit counsellor, or accountant before going this route. There are a number of ways to improve your rating, and a number of factors to take into account depending on your goals. It’s wise to get a second opinion before committing to one particular plan.

Talk to your creditors

If you’re struggling to make credit payments, or if you’ve fallen behind, you may be able to find some relief by contacting your creditors directly.

Talking to your creditors doesn’t cause any harm—you won’t be penalized for it—and your conversational skills as a therapist may come in handy when it comes to describing your challenges and appealing for help.

If you explain your challenges clearly, your creditor may grant you a temporary reprieve from late fees, which can give you some breathing room while you get your finances in order.

During a conversation with a creditor:

- Be transparent about your current financial challenges.

- Reiterate that you plan to pay the debt in full.

- Outline any plans you have for budgeting and ensuring you will be able to pay the debt.

- Record your conversation or take notes.

Write-offs for bad debt are a major operating expense for lenders. In the first nine months of 2024 alone, credit card companies wrote off $46 billion in debt. It’s in their best interest to make sure you’re able to pay your debt, or at least keep up with payments.

That being said, there may be nothing your creditor can do to help you. But at least you’ve made the effort, and during your conversations with creditors, you may be able to gain more insight into how to manage your debt or get help from third parties.

A note on debt settlements: Talking to your creditors, in this context, does not mean negotiating a debt settlement (reaching an agreement to pay less than the total amount you owe). Negotiating a debt settlement on your own is a complex and risky business. Most borrowers hire a debt settlement company to do the job for them. More on that below.

{{resource}}

Dealing with collections agencies

If you’ve fallen behind on payments, you may start getting calls or letters from a collections agency.

A creditor may use a collection agency to recoup losses on delinquent debt. They do that in one of two ways:

- Selling the debt to a collection agency at a discount, so the agency now owns the debt and has the right to collect it for you.

- Paying a collection agency to collect debt the creditor has been unable to collect for themselves.

Getting a call from a collections agency you’ve never heard from before, and finding out that you now owe them the total amount of your debt, can be scary. But there are limits to what collections agencies can and can’t do in the course of collecting debts, and steps you can take if they treat you unfairly.

Spotting scammers

Some shady individuals and groups make their money by collecting debts that don’t exist or by collecting debts from the wrong borrowers.

Other, legitimate debt collectors may try to bend the rules to their benefit or withhold information.

Every legitimate debt collector is required by law to provide you with the following information:

- Their name and mailing address.

- The name of the original creditor you owe money to.

- How much money you owe in total, with detailed information on interest, fees, and credits.

- Steps you can take if you don’t believe it’s your debt.

- Your debt collection rights, including the right to get information about the original creditor within 30 days of getting validation info from the debt collector.

If you get information about the original creditor, and you don’t believe the debt is legitimate (in whole or in part), write a dispute letter and send it to the debt collector by certified mail, requesting a receipt to show the letter was delivered.

You must send the dispute letter within 30 days of the collector providing you information about the original debt. Otherwise, the collector may assume the debt is legitimate and keep pursuing you.

Once you send them a letter, the debt collection agency is not allowed to contact you until they send you written verification of the debt. That may include a copy of the original receipt from the creditor.

What debt collectors can and can’t do

There are rules governing what collectors can and can’t do in the course of collecting a debt.

A debt collector may not:

- Threaten you. This includes threatening to suspend your driver’s license, have you arrested, or contact your employer. It also includes threats of physical harm.

- Lie to you. They can’t claim to be an attorney, say you owe more debt than you really do, or claim they’ll take legal action when they won’t.

- Harass you. A collector may not use obscene or profane language. They’re also not allowed to call you more than seven times in a seven day period. If you speak to a debt collector, they may not contact you again sooner than seven days after the call.

- Treat you unfairly. They can’t try to collect additional interest, fees, or charges on top of the amount you owe (unless a contract you’ve signed or laws in your state say they can). They may not deposit a post-dated check early. And they may not advertise your debt publicly. That includes mailing postcards or putting information on envelopes.

If a collector breaks any of these rules, stop communicating with them and report them immediately to your state attorney general’s office, the Federal Trade Commission, and the Consumer Financial Protection Bureau.

Reduce the impact of student loans

If you have student loan debt, it may make up a large portion of the debt you carry, and a correspondingly large portion of your monthly debt payments.

Finding ways to reduce your student loan obligation and monthly payments can help free up cash flow and reduce pressure on your finances. Here are the most common approaches and how they work.

Public student loan forgiveness

Following the end of the Biden administration in early 2025, the future of the public student loan forgiveness (PSLF) program is uncertain.

But if your loan is part of the federal student loan program, and if you work in government or for a non-profit, you may still be able to qualify.

To put it briefly, if you work as a therapist for state, federal, or local government, or if your employer is a registered non-profit, after ten years of employment you may be able to have your student loan forgiven. You’ll still need to make regular student loan payments during those ten years, however.

Does this help you if you already run your own practice? No. But if you’re considering making the jump from a government or non-profit position to self-employment, it may be worth taking into account.

Keep in mind that only 2.4% of applicants to the PSLF have had their debt forgiven, so it may not be worth your while to stay for 10 years at a job you dislike purely for a shot at debt forgiveness. Check out How I Paid Off $83,000 in Debt as a Social Worker and Single Woman for one therapist’s thoughts on the matter.

You can learn more about the PSLF from the Federal StudentAid website.

Income-driven repayment plans

If you have a federal student loan, and you’re not in default, an income-driven repayment (IDR) plan may help you to reduce your monthly payments.

IDR allows you to make payments based on a percentage of your discretionary income. The more you earn, the more you pay each month. And if your income is low, you make correspondingly low payments.

After a set period—typically 20 to 25 years, but for small balances it may be as short as 10 years—the remainder of your debt is forgiven. Your credit score is not impacted.

When you leave school, you get a six-month grace period before you start owing student debt payments. Automatically, you’re enrolled in a standard repayment plan—but at any time you may request to switch to an IDR plan instead.

To learn more about IDR plans and how to apply, check out the Federal StudentAid website.

Refinancing and consolidating student loans

If you have multiple student loans, or if you have a private student loan that doesn’t qualify for PSLF or an IDR plan—or if you have federal loans but still don’t qualify for these programs—you may be able to reduce monthly payments by refinancing or consolidating your student debt.

Student debt consolidation is like any other form of debt consolidation: You take out a loan at a lower interest rate than your current debts, pay off those debts, and then gradually pay off your new loan at the lower rate. It may be possible to include other, non-student debts in this consolidation. More on debt consolidation in the next section.

A wide variety of lenders offer student loan refinancing, which allows you to pay off your student loan with a new student loan at a lower rate. Be sure to do your homework before settling on a lender—there are plenty to choose from, and many different loan terms and repayment plans.

If you refinance or consolidate your student debt, you won’t be able to qualify for an IDR program.

{{resource}}

Get a debt consolidation loan

With a debt consolidation loan, you borrow a lump sum from a vendor equivalent to the total amount you owe for multiple debts. You then use the lump sum to pay off the debts.

There a few benefits to this approach:

- Less interest. Typically, a debt consolidation loan comes with a smaller APR than the average APR of the loans you use it to pay off. So, over the term of the loan, you end up paying less interest overall than you would if you paid off your debts individually.

- Lower monthly payments. Depending on the loan’s APR and term, you may end up spending less each month paying it off than you would if you paid off individual debts.

- Fewer monthly payments. If you struggle to keep track of your monthly credit payments, you may find it easier to make one payment per month (on your debt consolidation loan) than on multiple debts. This can also help if you’re creating a new household budget and trying to simplify your spending.

Depending on your situation, however, some features of a debt consolidation loan may cause problems:

- Fixed term. There is a fixed term to a debt consolidation loan. You must pay off the total loan during this period; otherwise, you could face serious financial consequences.

- Loss of collateral. If you secure a debt consolidation loan with a major asset—like your home—you could lose it in the event you default on the loan.

- Spiraling credit. If you use a debt consolidation loan to pay off creditors, but then continue racking up credit—for instance, continuing to accumulate credit card debt even after you’ve paid off credit cards with your loan—you could find yourself in a sticky situation: Not only are you now on the line for a large loan, but you need to make monthly payments on your new debt. Only take on a debt consolidation loan if you’re prepared to change your spending habits so it’s sustainable.

How to qualify for a debt consolidation loan

When you apply for a debt consolidation loan, the lender will check your credit score. They’ll also want to know your income, so they can calculate your debt-to-income ratio and ensure you’re able to afford loan payments.

Many applications for consolidation loans allow you to prequalify, meaning the lender will let you know whether you qualify before performing a hard credit check. To fully qualify, the lender must make a hard check, which will likely knock a few points off your credit score.

If you can’t prequalify for a loan now because of a low credit score, but you’re certain a debt consolidation loan is the right solution for you, you may be able to quickly improve your score and apply again. Paying off small debts to lower your credit utilization is one way to do this.

Debt consolidation and your credit score

Provided you’re on time with your loan payments, debt consolidation should not have any impact on your credit score. In fact, if you’re typically late making payments on the debts you’re consolidating, consolidating your debt with a more affordable loan (which you pay on time) could improve your score overall.

Where to get a debt consolidation loan

You have three main options when it comes to getting a consolidation loan:

- Banks, which typically offer the lowest interest rates on consolidation loans. However, they also typically require good or excellent credit (690+) to qualify. Even if your credit score isn’t great, it’s worth talking to the institution where you already bank to see what they have to offer for consolidation loans.

- Credit unions, which are less stringent than banks in terms of requiring a high credit score, but which may have less competitive interest rates. If you don’t already belong to a credit union, joining one is usually quick and easy. You may be required to make an initial deposit or share purchase, which is rarely greater than $25.

- Online lenders, of which there are many with widely varying requirements, interest rates, and terms. Do your research before choosing an online lender you’re unfamiliar with.

When to pay off debt with your retirement savings

If you’re particularly desperate to pay off your debts—or at least to substantially reduce them—you may have considered withdrawing money from your retirement savings to do so.

A word of warning: Paying off current debts with your savings for the future may not only reduce your chances of one day retiring, but could also impact your finances in the present.

If you withdraw funds from a tax-deferred account, they will be taxed as income at your current income tax rate. Your tax bill for the year will increase.

And whether or not your savings are tax-deferred, if you haven’t reached the age threshold for your retirement savings, you’ll likely pay an early withdrawal penalty. For instance, taking money out of your 401(k) before the age of 59½ years means paying a 10% penalty—and that’s before taking taxes into account.

Talk to an accountant or financial advisor before withdrawing any money from your retirement savings to pay off debt, so you can look at your options and decide whether it’s the right choice for you.

Some lenders may allow you to take out a debt consolidation loan, and then pay back the lender automatically redirecting your 401(k) contributions to them. This doesn’t affect the amount you already have saved in your 401(k), and it doesn’t result in extra taxes or early withdrawal penalties. But it could have long-term impacts on your savings for retirement. Consider getting professional advice before choosing this option.

Consider debt relief options for therapists

If you’ve taken steps to get your debt but you still can’t keep up with payments, it may be time to consider different forms of debt relief.

You have three main options:

- Debt management: Getting help from an accredited debt counsellor to manage your debt and eventually pay off the total amount.

- Debt settlement: Hiring a third party to negotiate with your creditors and (hopefully) have them reduce the total amount of debt you owe so you can pay it off completely.

- Bankruptcy: When you declare bankruptcy, your creditors write off your debt. However, your credit score will take a severe hit and your assets may be seized.

Here’s a breakdown of each.

Debt management

It could be the right choice if…

- You’ve tried managing your debt on your own without success.

- You have the resources (and desire) to pay down your full debt, but don’t know how to do it.

- Your largest and most problematic debts are unsecured (there is no collateral attached to them).

- Your debt-to-income ratio is 43% or greater.

Credit score impact

Debt management typically has a minor impact on your credit score.

Other impacts

You must close all current credit accounts and may not open any new ones while your debt is under management.

Where to go for debt management

There are many nonprofit credit counseling agencies that offer debt management plans. Make sure any plan you sign up for is accredited by the National Foundation for Credit Counseling. You may want to talk to several agents at different agencies before settling on one.

How debt management works

Typically offered by a nonprofit credit counseling agency, a debt management plan allows you to combine all your unsecured debts into one monthly payment, while also potentially paying less than you would if you paid each debt individually.

Here’s how it works:

- You provide detailed information about your financial situation to a debt management agent who then determines whether you are eligible for the plan.

- You sign up for the plan and agree to its terms.

- The credit counseling agency contacts each of your creditors and notifies them that the agency will now be making payments on your behalf.

- The agency seeks concessions from creditors, such as reduced interest rates and monthly payments and the suspension of late fees.

- You close any currently open credit accounts (you may be allowed to keep one open for emergency expenses).

- Each month, you make a single payment to your credit counseling agency that covers the total cost of your monthly payments.

- The agency makes monthly payments on your behalf.

A debt management plan typically costs an additional $25 to $40 monthly fee. In most cases, the reduction in your total monthly payments (due to concessions from creditors) more than makes up for the cost.

You should be prepared to commit to three to five years of debt management. Don’t sign up for a plan unless you’re certain you can make your monthly payments during this period.

And you should be prepared to live without access to credit during the duration of the debt management plan. (For many people struggling with debt, having zero access to credit cards and lines of credit helps to break bad spending habits and forces them to stick to a budget.)

Debt settlement

It could be the right choice if…

- You’ve tried all other options (including debt management) but still can’t keep up with your credit payments.

- You’re prepared to take a hit to your credit rating but you aren’t willing to declare bankruptcy.

Credit score impact

A debt settlement will have a moderate to serious impact on your credit report. Settled debts and delinquent accounts may remain on your credit report for up to seven years, which can make it difficult to secure debt in the future.

Other impacts

During the debt settlement process, your credit accounts may accrue unpaid interest and penalties, adding to the total amount of debt you owe.

You’ll also pay the debt settlement company a fee, typically charged as a percentage of each debt settled or a percentage of the total debt eliminated. And you may pay additional fees to open and maintain a savings account during the course of the settlement.

Where to go for debt settlement

There are many companies offering debt settlement. Unlike credit counseling agencies, these are for-profit ventures. Terms vary from one company to the next.

Any debt settlement company you consider must provide you with:

- Their fees, conditions, and terms of service.

- How long it will take (months or years) before your debt is fully settled.

- All possible negative consequences of settling your debt through the company.

- How much you need to save in a dedicated account before the company will offer settlements to creditors.

How debt settlement works

When you hire a debt settlement company, they negotiate with your creditors on your behalf to reduce the total amount you owe.

During these negotiations, you must stop making any payments on credit you owe. If your debt has gone to collections agencies, you may still receive calls from them during the course of the settlement.

That’s because creditors only consider it in their best interest to accept a settlement if it seems unlikely you’ll pay off the total debt. If you continue making payments, they’ll assume you’re financially able to service your debt, and will see no reason to accept a settlement.

While you’re working with a debt settlement company, and while you’ve stopped making payments on your debt, you deposit funds in a savings account. Only after these funds reach a certain amount—determined by the settlement company, and communicated to you before the settlement begins—will the company begin settling your debts.

Most companies charge a fee of 15% to 25% of the total amount you owe. The debt settlement company may only charge you this fee after they have settled your debts, and never before. You may need to pay additional fees to open and manage the savings account.

Debt settlement has the benefit of reducing the total amount you owe. If you’ve considered your options and you can find no other way of paying off what you owe, debt settlement offers an effective solution (short of bankruptcy) for paying off your debt.

You can expect debt settlement to hurt your credit score. It may also affect your future ability to borrow money. Settled debts remain on your credit score for up to seven years. During that time, potential creditors may be disinclined to extend your credit.

Finally, your creditors may not agree to the settlements offered by the company. (Some creditors won’t work with settlement companies at all.) In that case, you’ll be on the line for extra interest and penalties that accrued during the settlement process, and your credit score may be impacted as well.

The IRS regards forgiven debt as income, and you may need to pay taxes on it. Talk to an accountant before signing on for debt settlement so you can understand its impact on your taxes and decide whether it’s the right choice for you.

{{resource}}

Bankruptcy

It could be the right choice if…

- You can’t keep up with credit payments, and you see no way of eventually paying off your debts.

- Your total non-mortgage debt is 40% of your income or greater.

- You’ve considered all other solutions, including debt management and debt settlement.

- You’re prepared to virtually wipe out your credit score and begin building it up again from scratch.

- Assuming you no longer need to make credit payments (after they’ve been settled in the course of bankruptcy), you can afford to meet your needs without relying on credit.

Credit score impact

When it comes to credit score impacts, bankruptcy is about as bad as it gets. The good news is that, once your bankruptcy filing is complete, you can immediately start building up your score again.

Other impacts

Depending on which chapter you file under, you may lose major assets (your home, your vehicle) to bankruptcy. Other assets, like expensive electronics, jewelry, or clothing may also be up for grabs.

Records of your bankruptcy may remain on your credit report for up to ten years, making it difficult to be approved for credit in the future.

Your bankruptcy also becomes a matter of public record. Any interested party—including potential employers—may learn about your bankruptcy by searching Public Access to Court Electronic Records (PACER).

Where to go to file bankruptcy

While you can technically file for bankruptcy on your own, the process is long, complicated, and full of potential for making errors. If you plan to file, you should do it with the help of a bankruptcy attorney.

Bankruptcy attorneys charge their fees up front. For a Chapter 7 filing, you should expect to pay around $1,000 – $4,000. For Chapter 13, the numbers are closer to $2,000 – $6,000.

As part of a Chapter 13 filing, you enter into a plan to pay down your debts, which may include attorney fees for filing. For a Chapter 7, you should be prepared to pay the total amount in attorney fees before you file.

How bankruptcy works

Bankruptcy is a legal proceeding, and it can get complicated. This broad overview should help you decide whether it’s a route you’d like to take, but before making any major moves, be sure to talk to an accountant.

When you file for bankruptcy, some or all of your unsecured debt is wiped out. In exchange, you may need to surrender personal assets. Your credit score will also be severely impacted.

There are two types of bankruptcy filing individuals may choose from: Chapter 7 or Chapter 13. (Chapter 11 is reserved for businesses.)

Chapter 7 is the fastest, simplest method of filing, and probably closest to what most people think of when they think of bankruptcy. Your unsecured debts are wiped out after you file, and you’ll no longer receive calls from debt collectors. Liens on your income will also stop being collected.

Under Chapter 7, you’re required to report any major assets with cash value and surrender them. Depending on the laws of your state, you may be able to keep your primary vehicle, as well as any tools of your trade—that is, items you use in the course of earning an income as a therapist.

In order to file a Chapter 7 bankruptcy, you must pass a means test proving you would be unable to otherwise pay down your debt by filing under Chapter 13 instead.

Chapter 13 differs from Chapter 7 in that, rather than wiping out all of your debt, it significantly reduces the amount you owe. When you file under Chapter 13, you sign on for a three to five year payment plan during which you pay down the total amount of your reduced debt.

Chapter 13 allows you to hold on to your assets, so if you have valuable items you’d rather not surrender in the course of bankruptcy, this may be the better option for you.

Neither type of bankruptcy filing will wipe out student loan debt you owe.

Once you’ve successfully filed for bankruptcy, a certain amount of time must pass before you can file again. Namely, you can’t file a Chapter 7 if you’ve filed for another Chapter 7 within the past eight years, or a Chapter 13 within the past six years; and you can’t file a Chapter 13 if you’ve filed another Chapter 13 within the past two years or a Chapter 7 within the last four years.

Filing for bankruptcy should always be a last resort. Make sure you’ve exhausted all other options—and, again, consult with an accountant—before deciding to file.

—

Managing your debts is simpler when you earn a steady paycheck. But that can be tough to do when you run your own practice. Learn more about how to pay yourself as a therapist.

This post is to be used for informational purposes only and does not constitute legal, business, or tax advice. Each person should consult their own attorney, business advisor, or tax advisor with respect to matters referenced in this post.

Bryce Warnes is a West Coast writer specializing in small business finances.

{{cta}}

Manage your bookkeeping, taxes, and payroll—all in one place.

Discover more. Get our newsletter.

Get free articles, guides, and tools developed by our experts to help you understand and manage your private practice finances.